Bitvana or the bitcaust

"It's all money. Always has been."

Nobody has any respect these days. But I feel that since I was writing about the game theory of hyperbitcoinization in 2006, folks should have some respect for my opinions.

At least on that subject. Ya know. But now it’s 2023 and everyone is talking about it. So let me explain how—in nit can and can’t happen.

But first, lest I pump you unduly with this hyper-bullish take, let me scare you into panic with a hyper-bearish theory of debitcoinization. (The only way to write about finance is to be either neither bull nor bear, or both. No one wants to hear it—but anything else feels sordid. And actually, all this is not even finance—just Austrian economics.)

The possible bitcaust

The primary theory of debitcoinization is that the government will make it impossible to legally sell crypto for dollars. Here is a thread about how plausible this seems, right now, to serious crypto lobbyists.

Fortunately or unfortunately, as a secondary effect of this policy—now dangerously close to plausibility, thanks to the immense nest of scammers that infested the space, and hence the understandable desire of influential venture capitalists to put all this behind them and invest in some AI-powered dog sweater that lets Rover speak English—it will no longer be possible to illegally sell crypto for dollars.

Rather, sellers will exceed buyers at any price—as for any fully discredited security—and in any market—from the heart of Wall Street to the slums of Caracas. Nothing like this has ever happened in any previous crypto crash followed by a recovery. This is power’s final answer to the bitcoin question—a bitcaust.

As for any fully discredited security, few of the bagholders will blame the regulators. Their order of blame will be: (c) the regulators; (b) anyone who profited; and (a) themselves. Power is a hard schoolmaster, sparing rebels not the rod. Anyone is a rebel if he fails.

This is the true cryptocalypse. All it would take for this to happen tomorrow, so far as I know, is a few raids and/or regulatory actions against a few small banks—and it will be impossible to transfer dollars in any scalable, legitimate way out of crypto. But the best case against it this happening tomorrow is that I predicted it twelve years ago.

The result of a cryptocalypse would be the destruction of a trillion dollars in global net worth, with nontrivial macro effects. Moreover, this trillion has a higher propensity to spend than most of the investor wealth that gets destroyed—so there will be proportionately macroeconomic effects. Deflationary effects. This money that people thought they had, was not money, and now cannot be spent. Sad!

Well: nothing a little stimulus can’t cure—Covid had deflationary effects, too. Or would have. Before Washington unleashed vast fleets of Apache attack helicopters darkening the sky with dollars. Now we know helicopter money works!

(The clever way to shut down crypto without deflation or political blowback would be for the Fed to both ban and buy back all crypto. If you have crypto, send it to the feds. They will figure out if you are a criminal. If not, they will pay you for it, in new dollars, at the closing price. Since we do not live in a clever world, nothing like this could possibly happen.)

Till now, the main shield of the crypto world has been the image of “blockchain,” a genuinely revolutionary new technology—but one which our political and economic system may be no more ready for, than the Roman Empire for semiconductors. The blockchain, a work of genius, was perhaps made for a freer, safer world than ours.

Standing behind this shiny image is the passion of a new populist investing class—in numbers which carry significant weight both economic and political. This political battle is the real battle. The combination of low-class mass and high-class hype has been invincible—up to now. But as we’ll see, crypto only needs to lose once.

I must emphasize that any decision to murder crypto is a political decision. So it must be taken by bureaucrats, not politicians. While the bureaucrats are still scared by large numbers of souls, recent events have hardened their hearts.

Now, due to the failure of FTX, there is now an anti-Bitcoin lobby—a constituency for a lethal strike on crypto as an industry. Of course the press has been trying to gin this up for ages—now they have powder in their guns.

Also, when they look at this shiny new thing, they still see little organized, legitimate productive activity. Also, there is a banking crisis on—if you want to settle a score with your cousin, chaos in the streets is a great excuse—no one will notice another corpse on the sidewalk.

Well… okay… it’s 2023. Here is something I wrote about Bitcoin in 2011:

I’ll be frank with you, dear reader. When I came up with the MoMT, my first thought was: how can I, Mencius Moldbug, make some damned money from this?

As system software is my first love, it was not that hard to think of an answer. In some ways Bitcoin is actually much better designed than my design, which was not distributed. The use of Lamport hash chaining is particularly elegant.

I did not wind up building my design, however, because I sensed a problem. Bitcoin has the same problem, but worse.

The basic economic design is the same: an artificial currency of limited supply. What is the currency backed by? Nothing but speculation and hot air. Note that this (contrary to its exponents’ claims) violates Mises’ classical “regression theorem.” MoMT has no problem with an unbacked monetary candidate, because the required epsilon can be provided simply by the probability that the monetary system is adopted.

If Bitcoin becomes the new global monetary system, one bitcoin purchased today (for 90 cents, last time I checked)1 will make you a very wealthy individual.

Obviously we are not all the way there—but we are farther than I can imagine. The reason I wrote this post 12 years ago and did not buy any bitcoins for $0.90, apart from being (a) stupid and (b) broke with two small children, was this—from the same post—the problem:

Because we’re governed by dumb people, here is what I think will happen with Bitcoin.

Stage 1: Bitcoin does not exist. Stage 2: Bitcoin exists, but is worthless. Stage 3: Bitcoin exists, and is used by strange and desperate weirdos and geeks. Stage 4: Bitcoin is used by Slashdot readers, perhaps slightly less desperate. (You are here.) Stage 5: Bitcoin is used by criminals. Stage 6: All Bitcoin exchanges are shut down by USG. Stage 7: Bitcoin exists, but is worthless. Stage 8: Bitcoin does not exist.

At least on the surface, Bitcoin exchanges violate the critical know-your-customer rule which USG enforces on all money-transfer businesses. As a money-transfer business, you are essentially an agent of the government—a spy. To a regulator, Bitcoin seems like a way to transfer arbitrary quantities of money anonymously. This is a nonstarter, and the regulator knows exactly whose necks he has to squeeze—the spies who are not doing their jobs.

He cannot shut down Bitcoin itself. He can trivially shut down Bitcoin–dollar exchanges, or even Bitcoin–gold exchanges. Probably seizing all their dollars, etc. He probably can’t seize their bitcoins, but it doesn’t really matter.

To save in a currency is to place your trust in that currency. If you put energy into this great collective battery, you have to be able to get it back out. If that trust can be convincingly damaged, the currency has no chance. If people lose money in bitcoins, the currency can never recover. No one will ever again exchange it for dollars, or even alpaca socks. It will be dead. Its chances, now and forever, will be zero—not even epsilon.

Slashdot! That was me in 2011. I would add a “Stage 4.5: crypto is worth a trillion dollars and has Super Bowl ads.” I would actually be rich if I had noticed that Stage 4.5 would happen, and last for years. Champagne to all those who were smarter! But…

Here, in 2023, is a government warning, from all bank regulators, to all serious players in banking, that they should stay out of crypto—at risk of their companies and careers:

The agencies are continuing to assess whether or how current and proposed crypto-asset-related activities by banking organizations can be conducted in a manner that adequately addresses safety and soundness, consumer protection, legal permissibility, and compliance with applicable laws and regulations, including anti-money laundering and illicit finance statutes and rules.

Based on the agencies’ current understanding and experience to date, the agencies believe that issuing or holding as principal crypto-assets that are issued, stored, or transferred on an open, public, and/or decentralized network, or similar system is highly likely to be inconsistent with safe and sound banking practices.

Further, the agencies have significant safety and soundness concerns with business models that are concentrated in crypto-asset-related activities or have concentrated exposures to the crypto-asset sector.

We find that crypto is a vast hive of scum and villainy. To the extent that there are legitimate players, they make all their money from illegitimate players. So, if you have any connection to crypto, don’t be shocked when we shoot you in the head.

This is why, when the thin link between crypto and money is this kind of bank—the kind that prefers to ignore a warning as clear as the above—it is okay to get antsy. At this moment, there has never been a better time to shoot a shady bank in the head.

What happens if Coinbase is cut off from banking? FTX was a total scam; Coinbase is a completely legitimate company—the only really, deeply, compliant exchange. Once CB cannot bank, the precedent is set—no one in crypto can touch the banking system. Forever. And as we’ll see, it doesn’t even need to be forever.

Once Coinbase cannot bank, everyone with a Coinbase balance gets exactly the FTX experience: they cannot touch any of the money they had yesterday. This is not because Coinbase is shut down, but because it cannot send them dollars. It can hold USDC in their name—it cannot get green paper to come out of their ATMs.

As for stablecoins and other asset-backed coins, there are two kinds: legitimate, like USDC/Circle; funky, like Tether. While USDC is more serious about blacklisting, all these coins have circulated freely through the black economy. The regime will seize their assets and use them to allow non-criminal coinholders to be made whole. Any criminal funds will be confiscated and remitted as reparations to Black Lives Matter.

The result of this is that everyone will be looking for anyone to sell their BTC, just as everyone now who holds FTT (the FTX “stock” token) will be looking to sell their FTT. What is the price of FTT? Is it zero? It is not even zero. There is no price—there is a nominal price, but there is no liquidity. But once there is no liquidity in anything as big as BTC, there will not even be a quote. The sites themselves will disappear.

Not only will anyone legitimate not find any buyers—since they don’t know how to even connect to illegitimate financial networks—the illegitimate networks will also try to sell their BTC if they can. And who will be buying it? No one illegitimate… why would they? Criminals, when handling money, are actually very conservative. And criminals have no collective solidarity whatsoever.

The whole crypto financial system remains parasitic on the legitimate financial system—there is no end-to-end chain of production in the crypto economy. For example, in the whole world of centralized (CeFi) and decentralized (DeFi) crypto lending, there are/were no real borrowers—no one was financing a factory or even a house with crypto. At most they were financing crypto mining. But mostly, they were financing Ponzis.

The narrative will be that crypto as a whole was a scam and a joke all along. It got big—the bigger you get, the harder you fall. Lol.

The truth will be—and this is the truth of many rebellions that fail—it could have worked. It just didn’t, because of people—and the very specific choices that they made.

What I realized when I thought about it twelve years ago was that as Bitcoin/crypto (one bad choice was either making Ethereum its own competing store of value, and/or not giving Bitcoin a contract engine) expanded, it would have political consequences.

In fact, if the bubble that would become money got big enough, it would compete with the state—in fact, a bet on the bitcoin economy would become a bet against the state. And this bet would be a self-fulfilling bet—the more people believed in it, the more likely it would be to succeed.

Fortunately or unfortunately, self-fulfilling bets are also fragile. If power can massively smash the army of bettors, massacring them and/or putting them to flight, it can easily reverse the whole dynamic and replace the mass excitement with mass revulsion.

The question then was when the immune system of the state would become activated. While in 2011, due to being an idiot, I wildly mis-assessed the timeline, I foresaw that the first stage of this conflict would be a conflict between criminal anarchy, not goofy libertarian anarchy, and the bureaucracy.

And in this conflict there was no chance that the criminals would win. Finem respice. There is nothing criminal about Coinbase; it would just be collateral damage. The lump doctor always likes to leave “clean margins.” Coinbase is now said to be looking around for overseas banks “in high-bar regulatory jurisdictions.” Needless to say, all serious First World bankers would come to work naked if Washington so ordered. So…

If you find all these facts and logic all too convincing, and want to sell because of it— first, take a deep breath and remember: I’ve been predicting this cryptocalypse for twelve years, and it hasn’t happened yet. So I am probably just full of shit. Right? Right?)

The road to Bitvana

Now let’s assume that (perhaps due to the eternal secret financial power of us Jews) Cross River Bank, or some other slender lifeline of legitimacy between legitimate crypto and legitimate banking, survives.

(Of course, my 2006 theory was originally developed for gold, and applies as least as well to gold. Which is a lot harder to kill. In any case, posit an unkillable Bitcoin…)

In 2023 it is now much easier to see the road to Bitvana—to a world in which Bitcoin is the universal numeraire and monetary standard, in which all prices and all financial assets are denominated in Bitcoin. Bitcoin has already gotten most of the orders of magnitude it needs—but the last three are the hardest.

(Ethereum could still overtakes Bitcoin in the race for monetary standardization—which is still possible—proof-of-stake coins are more susceptible to outside pressure, but leak way less money—a semi-stable “bimetallic” standard, like the old gold/silver system, may also be possible—but let’s suspend this conversation for simplicity.)

There are two theories of hyperbitcoinization. Unfortunately, the leading theory is just plain wrong, and a trap. Why would all these super-smart coin people believe this wrongness? Well—a parable.

The parable of the hyperpope

The planet Thear, a trillion light-years away, is ruled by a hyperpope. The hyperpope, through his magic hyperhat, can speak to God 24/7 and is also immortal. So is his absolute and beneficent rule of the happy planet of Thear.

Only one thing can end his eternal reign: the birth of a russet two-headed heifer. On this birth, God will act! The mutant cow’s owner becomes the new hyperpope.

The truth is that the hyperpope is just a dude and his hat is just a hat. He appears to be immortal because he clones himself. Each clone appears in public only between the ages of 25 and 30. Also, as an absolute caesaropapist dictator, he does… awful things. This infamy must end!

Among the underground rebels who aim to end the hyperpope’s abominable reign, there are two strategies. The first strategy is to spread this dangerous truth about the hyperpope. The second is to… genetically engineer a russet two-headed heifer.

The false theory of hyperbitcoinization

The meaning of the parable is that if you want to overthrow a regime, your first step is to stop believing in it. If you want the real Bitvana… you need to believe in reality.

If any of the legends of the regime are stuck in your brain, they will probably lead you to bad, ineffective strategies for overthrowing it. Even worse, it might lead you to bad, ineffective theories of how it will overthrow itself. (You could just wait for the heifer.)

When people tell you the dollar is about to collapse, etc, they are into the false theory. Believing in the financial hyperpope corresponds to taking graphs like this seriously:

This is a graph of M0—the monetary base. This is the number of actual dollars. When people use metaphors like “printing money,” they are believing in the hyperpope—as we’ll see below.

By criticizing the Fed in language that inherently repeats the Fed’s own propaganda, they are not attacking the system—they are stabilizing it.

As the previous post on informal securities discussed, your bank “deposit” is not an actual dollar. It is a bundle of (a) a zero-term, continuously renewed loan, of an actual dollar, to the bank, and (b) a credit default swap, on the bank—“deposit insurance.” The sum of all “deposits,” plus M0, is M1—bank money.

Above 250K, your credit default swap (b) is an informal security—an unwritten promise that economies in practice depend on, like property rights in a Third World slum. Moreover, below 250K, you are still banking on an informal security. FDIC’s promise to bail out your bank is formal—but the Fed’s promise to bail out FDIC is informal. Whoa.

Believing in the hyperpope is believing our banking system is a free-market economy. In a free-market economy, informal securities do not exist—because informality is the flexibility of power to do whatever the hell it wants.

If you believe these informal securities do not exist, you must believe there is a hard line between M0 and M1. If there was a hard line between M0 and M1—for example, if the Fed repudiated its informal option to FDIC, or FDIC repudiated its formal option to the banks—everything would explode. Since everything does not explode, there is no such hard line.

The “monetary base” used to be the “gold reserve.” No one can print gold. We are no longer on the gold standard, but we have many paper systems designed for it—and we have a lot of language to think in terms of it. Thinking in this language is believing in the hyperpope. Paper is not gold and does not work like gold at all.

Generally, the language of the 20th-century financial system makes us think the lie that there is a hard line between M0 and M1. When we talk about the Fed “printing money” when M0 increases, with dramatic curves like the above, we are talking as if M0 was gold and the Fed had found the philosopher’s stone. It isn’t and it hasn’t.

In fact, M0 is USG equity—government stock—and M1 includes options on USG equity. When we calculate the “money supply,” which means calculating the number of USG shares outstanding—the fully diluted equity—we need to include all the potential shares USG has written—including all these informal options!

For the market value of these informal options can only be defined by asking the question: what would happen to markets if all informal options were repudiated?

In that world, only a few trillion in real USG dollars would exist to repay over a hundred trillion dollars in financial promises denominated in… real USG dollars.

The market price of these promises (debts, bonds, stocks, etc) would… rapidly decline. Indeed, they would perform what Elon Musk calls a “rapid unscheduled disassembly.”

The difference between the price of these promises with and without the stealth options is USG’s hidden equity. Like some skeezy company in Panama, USG has issued way more shares than it wants you to know.

The reason “printing money” is a bad metaphor is that almost all new USG equity is not issued as formal securities! It is conjured into being as a sort of virtual particle through the potential power of creating formal equity.

Suppose USG were to issue “Monopoly default swaps” that allowed you to take your Monopoly money (pre-1991 Parker Brothers sets only) to the bank and trade it for real money. No one would need to trade in their old Monopoly money. They could just spend it. But since no one traded it in, no new dollars would literally be “printed.” The Fed could do this for Beanie Babies or old bottle caps or anything else.

Inflation explained

Unlike any company, USG is a sovereign. The profit and loss of a sovereign company is its balance of trade; the capital is its land and people.

Historically, the stablest sovereigns both trade and save in an exogenous currency, such as gold or Beanie Babies. A sovereign company whose people must save in its own sovereign equity is weird; one which buys imports in its sovereign equity is weirder. The former is as if Microsoft made an online game whose currency was MSFT stock. The latter is as if Microsoft bartered MSFT stock for office chairs.

And if there were banks in the online game, and if Microsoft “insured” those banks—maybe only up to 100 shares—we would have a lovely replica of the USG system. Hopefully this simple metaphor removes some of the ancient mystique of the Fed.

Per Milton Friedman, inflation is always and everywhere a monetary phenomenon. Shills and fools insist on mismeasuring it so they can smuggle money out the door. Most of the liabilities of the banking system—measured by the simple “crash test” above, in which informal securities are repudiated—are these informal securities.

Nor does informal value end at banking’s edge. Everyone on Wall Street has heard of the famous Fed put, which used to be the Greenspan put. For those without a finance background, Wikipedia’s description may be evocative:

The term “Greenspan put” is a play on the term put option, which is a financial instrument that creates a contractual obligation giving its holder the right to sell an asset at a particular price to a counterparty, regardless of what is the prevailing market price of the asset, thus providing a measure of insurance to the holder of the put against falls in the price of the asset.

While Greenspan did not offer such a contractual obligation, under his chair, the Federal Reserve taught markets that when a crisis arose and stock markets fell, the Fed would engage in a series of monetary tools, mostly via Wall Street investment banks, that would cause the stock market falls to reverse. The actions were also referred to as “backstopping” markets.

Informal securities for everyone! Well, at least, every stockholder. Informal securities for the rich! And the middle class too. No wonder our “free-market economy” is tech plus ag/energy/minerals, plus hospitals, universities and government, plus a hollow shell of FIRE. It has been bloated on soy and cheap loans for a century and change. Drive across America and you’ll see the rotting, burned-out result.

Of course, the Fed does not need informal instruments to manipulate stocks. When it sets short-term interest rates, it manipulates the price of all long-term assets. When it sets long-term interest rates (by quantitative easing/tightening), it sets the price of all long-term assets—fixing the whole yield curve. The bond vigilantes have not been seen in 30 years, nor the gnomes of Zürich in 50. Much capitalism! Such free market!

Furthermore, setting interest rates adjusts the price of tangible capital assets—notably our good friend real estate. When your house was going up 100K a year—was it becoming a better house? Was that linoleum in the kitchen healing? Of course not. It was all just the Fed, piping informal securities into the attic.

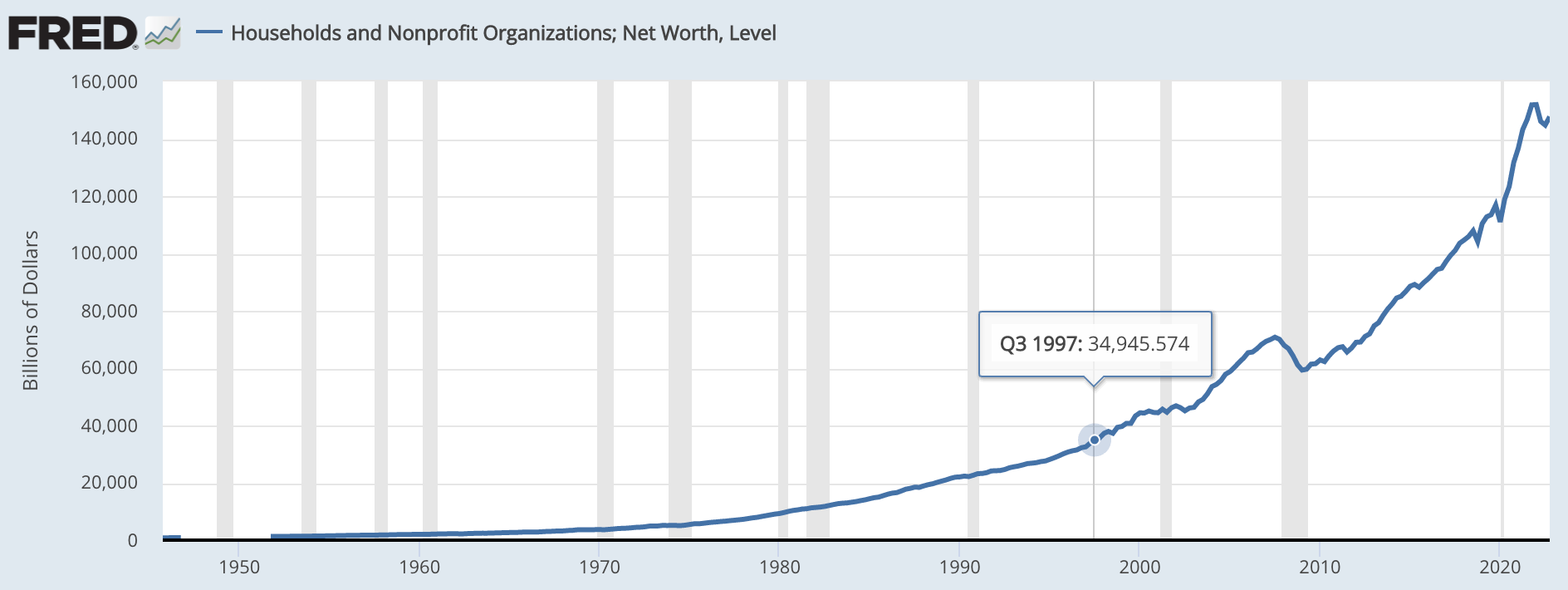

It’s all money—always has been. If we imagine two new “monetary aggregates,” M6 and M7—M6 being all financial assets, M7 adding all financed assets—we might see a curve that looked something like this one:

This graph, I believe, is the best metric of “inflation” we have. Inflation is a function of too much spending power “chasing” too little productive power. The spending power of the consumer is the total net worth of the consumer—which is this graph. Note that dips and flats in the graph mostly match those mysterious space storms of the credit system, our “recessions,” shown as the gray bars.

Prices are a function of consumer demand—measured in “nominal” dollars. And consumer demand depends on spending power, which is personal net worth. It may depend slightly on the asset allocation of the consumer—but does your spending really change depending on whether your portfolio consists of stocks, bonds or cash? Even literally illiquid assets like houses influence spending indirectly.

Note that this “M7” aggregate is like 30 times the size of M0. This is why people who point at graphs of M0 and talk about “printing money” are completely out to lunch. Inflation is always and everywhere a monetary phenomenon, that is, a function of spending, that is, function of net worth in dollars; a dollar of net worth is a dollar.

Why has this whole curve gone up like yeast since 1950? Was it actually because our cars got more reliable and our TVs got sharper? Why does that require increasing dollar-denominated net worth? Maybe some of it is population increase—why should even increasing population require more and more and more dollars? This is not even economic reasoning—it is just sympathetic magic.

It’s all money. Always has been.

Repudiation and recognition

The three horsemen of Third World finance—informality, discretion and uncertainty—are inseparable. All of the Fed’s power is its discretion to “backstop” markets with infinite dollars—just as Microsoft in the above example could backstop its in-game financial markets with infinite potential MSFT shares—to insure banks, set interest rates, and so on.

Everyone is supposed to think the Fed’s discretion is the cure for financial crises. It is, of course. It is also their cause. A duration-matched financial system without informal securities will not need any discretion or uncertainty; it will be stable without any systematic price fluctuations, inflation, deflation, credit crashes or business cycles. Dear future: try it and see.

The vast power of the Fed becomes visible when we imagine it repudiating all its informal promises—many of which, through the magic power of swap lines, have wound up financing things like Indonesian palm-oil plantations. In dollars.

Think about all the dollar debt in the world. Now, think about the size of M0. Think about the game of musical chairs that ensues when 5 trillion dollars have to pay off 100 trillion dollars in debt.

You can call this a “dollar collapse” if you want—but it would be hyperdeflation, not hyperinflation. And it would be global. Grown men in Cambodia would murder each other for a quarter. A few thousand bucks would buy an island in the Seychelles. And an island, indeed, would be a good place to be.

The unstable dollar economy is always about to collapse. Without informal action, it will collapse—instantly. But only downward. And this will never happen, because no one has any reason to let it happen—as we saw during an exogenous crisis, Covid. Look on the graph above to see how much “value” Covid created.

Think of the dollar financial system as a wingsuit jumper doing proximity flying. It always looks like the wingsuit is about to crash into the ground—and sometimes, mistakes are made and this happens.

Actually, when you fly that close to the ground, you are using every control surface you have to push the suit down. This means that if you screw up anything, you fly up into the air. Similarly, any failure of informal securities makes the dollar skyrocket, in a so-called “dollar shortage.” (Free-market economies do not have “shortages.”)

The correct way to formalize all these informal securities is to recognize them as real—like turning informal property rights in a Lima slum into real title deeds. This will be neutral for private net worth

While this is easy for bank money—it effectively means recognizing that all banks are branches of the Fed—it is much trickier for tangible assets. With a stock or a house, there is no way to measure or define the contribution of monetary policy to valuation.

The only way to reset these monetized assets to market prices, without damaging everyone’s private net worth, is to nationalize them all at the market price, fix the supply of money, and auction them back to the new free market—presumably at a lower price. This will result in a moderate one-time increase in private net worth.

The true theory of hyperbitcoinization

The true road to Bitvana is simple: it is the Schelling point of capital flight.

The best way to conceive the nation of Bitcoin hodlers is as a nation: Bitstan. The new reason to move your money to Bitcoins in Bitstan, if you are an American in the 2030s, is the same as the old reason to move your money to gold in Switzerland, if you are an American in the 1930s.

What is the motivation of capital flight? There are three motivations of capital flight: two push (capital dilution and capital destruction), and one pull (capital compression).

Dilution in a company is an increasing quantity of shares—formal or informal. As we have seen, the best measure of a sovereign money supply on a fiat system like USG’s is just consumer net worth. The more everyone’s portfolio and house goes up, the more dollars are chasing the same number of goods. Rising house prices dilute your dollars, and not just dollars used to buy houses.

Destruction is when your risky assets fail—effectively impossible for bank money, but quite possible for stocks and houses and the like. In the expansion phase of the cycle, risk assets are where money wants to be—they “grow” the fastest. In a recession, money retreats to the banks, where it earns zero interest, and risk assets lose money. Isn’t this game fun? Deflation/recession increases the value of your dollars, but only if you can shuffle them around fast enough.

Compression is when everyone buys bitcoin and that makes bitcoin go up. Or when everyone buys gold and that makes gold go up. There is still a lot more gold, by value, than bitcoin… so the more people who know the theory, the more people who profit.

The key point about capital flight is that it is only a Schelling point if the end stage is stable. If all rich people’s capital goes to Bitstan, for instance, what does that do to the economy of Bitstan? Capital flight normally goes to countries with a trade surplus—but what does Bitstan export? Bitstan, in fact, leaks money—not least because mining creates forced sellers (perhaps an Ethereum flippening would help)…

Capital flight is a thing in boom or bust, because dilution is a thing in the boom, and destruction is a thing in the bust. And compression is always a thing. So…